Introduction

UK wholesalers, food importers, and suppliers are increasingly under pressure from complex payment workflows, rising fees, and cash‑flow uncertainty. If you’re managing payments, reconciliation, and supplier relationships, these issues can hold your growth back. In this post, we explore the primary payment challenge of late or inefficient payments, along with four more critical obstacles — and how the right fintech‑ERP integrated platform can help smooth operations and protect your margins.

'

1. Late payments and cash‑flow crunches

One of the biggest pains for UK suppliers is simply waiting too long for money to arrive. According to a recent UK survey, 51 % of B2B invoices are currently overdue. Atradius+1

Delayed funds mean you may struggle to pay your own suppliers or staff, borrow more, or invest in growth. Higher procurement costs and market uncertainty are key drivers. Procurement Magazine

Use‑case scenario: A food importer delivers to multiple retail outlets but is paid 45–60 days later; meanwhile the supplier’s stock costs and delivery charges must be covered immediately, squeezing their working capital.

2. High processing fees and payment cost inefficiencies

Many suppliers are paying too much in card fees, legacy bank transfers, or third‑party intermediaries – reducing margin. One UK business payments report highlighted “high fees” as a common pain for SMEs. Ecommpay+1

Use‑case scenario: A wholesaler receives many payments by card or via manual bank transfers that incur charges or delays; margin erosion increases, and there’s no unified view of cost per payment.

3. Manual reconciliation and complex payment workflows

When payment methods are fragmented (bank transfer, cheque, card, open banking link) the reconciliation effort becomes heavy and error‑prone. A UK report noted that complex payment setups – fluctuating volumes, multiple methods – challenge SMEs. News Events Insights

Use‑case scenario: An import company receives a mix of payment types from clients; each payment must be matched to an invoice in the ERP, taking finance team hours every week and delaying insight on cash unlocking.

4. Poor visibility of incoming and outgoing funds

Without real‑time visibility into incoming payments or cash outflows, forecasting and working‑capital decisions suffer. The Open Banking Ltd guide notes that open banking gives businesses access to up‑to‑date financial data and better cash‑flow control. Open Banking

Use‑case scenario: A supplier doesn’t know when a large retail customer will pay or whether any payment has failed until days later, making inventory planning and next‑order decisions tricky.

5. Fraud risks and payment method vulnerabilities

As payment methods evolve, fraud risk grows. UK businesses face increasing risk from scams, chargebacks and push‑payment frauds. Ecommpay+1

Use‑case scenario: A mid‑sized importer receives what appears to be a valid payment but the payer account is compromised or the transfer is reversed; the supplier is left with goods shipped and no payment.

Solution: How fintech + ERP integration solves these challenges

The five challenges above can be addressed by combining modern payment technology (notably open banking payments) with a tightly integrated ERP system. For example, with Zendr, you can process account‑to‑account payments instantly and manage your entire wholesale operation from one secure platform.

Here’s how:

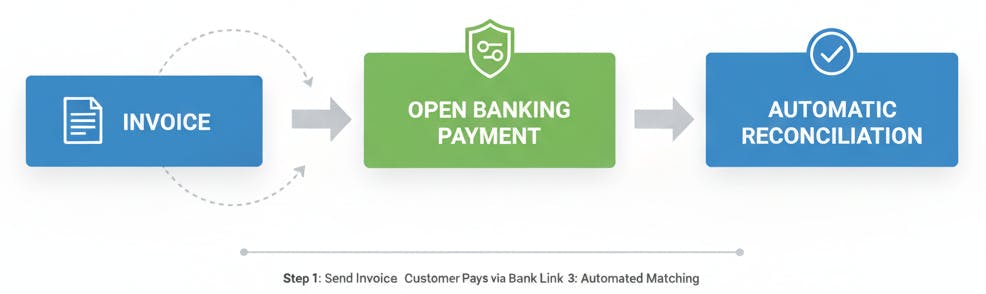

- Faster receipt of funds — using open banking payments means clients can pay you directly from their bank account, often in near real‑time, reducing delays. sotpay.co.uk+1

- Lower cost per payment — bypassing card networks and reducing intermediaries means lower processing fees for your business.

- Automated reconciliation — payments sync directly into your ERP system; invoices are marked as paid automatically; less manual checking.

- Enhanced visibility and forecasting — all payment flows (sales, refunds, supplier payments) appear in one dashboard, giving you accurate cash‑flow insight.

- Improved fraud defence — open banking payment flows reduce reliance on cards, lower chargeback risk, and benefit from strong payer authentication.

- Supplier‑friendly operations — smoother payment experience leads to stronger relationships with your clients and partners.

Benefit or Deep Dive

Here are measurable benefits your business can realise by tackling these payment challenges:

- Time saved: Reduce payment‑reconciliation time by 70–90 %

- Cost reduction: Slash card/transfer fees by up to 30–50 %

- Cash‑flow improvement: Get paid days earlier on average, freeing up working capital

- Forecast accuracy: Real‑time visibility means fewer surprises and smarter buying/inventory decisions

- Risk reduction: Lower chargebacks and push payment fraud incidents

- Supplier relationships: Better payment experience strengthens loyalty and improves retention

Zendr’s Approach

At Zendr, we understand your business as a UK wholesaler, importer or supplier. Here’s how we help you directly:

- You sign up → connect your bank and ERP system

- You issue invoices via our platform or sync from your existing ERP

- Your clients receive an instant payment link or an account‑to‑account option

- Payments arrive and automatically post in your ERP; you receive alerts if any payment fails or is delayed

- You access dashboards showing upcoming payments, settled transactions, payment methods used, and cost per payment

- You maintain a full audit trail, reconcile effortlessly, and free your finance team from manual tasks

Whether your business is dealing with dozens or hundreds of payments each week, Zendr scales with you — offering flexibility, speed, and control.

Conclusion

UK suppliers face significant payment challenges: from late payments and high fees to manual reconciliation, limited visibility, and fraud risk. By adopting open banking‑enabled payments plus ERP integration — as provided by Zendr — you can transform how you get paid, manage cash‑flow, and operate efficiently.

Join hundreds of UK wholesalers transforming their payments with Zendr.